I have had a theory about what’s going on in future facing metals for a while…but haven’t voiced it in case I sounded like I was wearing a tin foil hat.

But as time goes on I become more confident in my view, especially after a managing director of a $3.5bn stock announced the same view at an AGM yesterday.

According to The Australian, Iluka Resources [ASX:ILU] managing director, Tom O’Leary, ‘launched an astonishing broadside at China’s control of the rare earths market, accusing the world’s dominant critical minerals player of brandishing its power over metals supply and pricing like a weapon’.

He went on to say, ‘it is this monopolistic production, combined with interference in pricing, that is resulting in market failure’.

If China wants to scare off any competitors in the West from challenging their hegemony over critical minerals, what better way than to force the price down to a level that sends competitors broke?

China has ramped up synthetic graphite supply massively. This has led to a serious fall in prices of both natural and synthetic graphite. China also banned the export of many graphite products late last year.

China is behind the huge supply increase in Indonesian nickel that has collapsed the price and forced the closure of many nickel operations in the West.

In the rare earth market that China has a stranglehold on, the price is at levels that ensures no one is making money, according to Tom O’Leary.

When the price of a commodity falls deep into the cost curve, astute investors start to buy the strongest companies in the sector. Because the price can’t stay below the cost of production for long before supply collapses and the market gets back into balance.

Despite the bearish outlook for electric vehicle demand in the short-term, the long-term story remains intact. Strategic minerals like rare earths are also used in defence applications and renewables such as wind farms.

The future demand profile for rare earths is heading much higher over the next decade regardless of short-term pricing woes.

If China is behind a concerted effort to force the price of future facing metals and minerals well below the cost curve to scare off competition it increases my confidence tenfold that we are entering a period when investors should be loading up on the best companies in the space that could reap the rewards when prices recover.

If you are in a pool and holding a large beach ball and try to push the beach ball down into the water, what happens when you let it go?

That is how I see China’s efforts to crash markets it has cornered to scare off competition. They can’t hold the beach ball down in the water forever.

The West has been caught napping at the wheel over the last decade and is playing catch up at the moment, trying to build an industry in critical minerals outside of problematic regimes such as China and Russia.

Hopefully Western governments will become aware of the games China is playing and will support efforts by market players to get projects up and running.

The recent US$533m package the federal government offered to Arafura Rare Earths [ASX:ARU] is an example of what is needed.

A situation like this is exactly the type of conditions I like to see as I hunt for opportunities.

I like to focus in on sectors that I think have a good chance of flying higher based on a combination of strong fundamentals and technicals.

When both meet, the best situations arise.

Then I zero in on the best stocks in the sector and even consider recommending a sector ETF to gain exposure to the biggest stocks in the sector in one trade.

That approach worked out well last year when members of Retirement Trader jumped on a uranium stock and a uranium ETF just before the uranium price blasted off.

The uranium stock has jumped 110% above the entry price less than a year ago and the uranium ETF is 73% above the entry price over the same period.

If you have been watching my Closing Bell videos you’ll know that I also picked the recent breakout in the gold price. A couple of months ago members of Retirement Trader got three buy alerts for gold stocks that have rallied strongly.

One is up over 40% above the entry price, another is 22% above the entry price and the straggler has popped 5%.

And while not all stocks in these sectors will perform like this…

Achieving those returns wasn’t rocket science. It is just a methodical approach to find sectors that have a strong fundamental story combined with an exciting technical set up.

Then zero in on key stocks in the sector or invest in the whole sector via an ETF.

I picked two of the best performing sectors over the last year following that approach and I reckon I’ve found the third which is close to setting off a buy signal.

The rare earth sector mentioned above is getting close to confirming a buy signal but has more work to do before I will get excited.

The sector I am interested in isn’t being cornered by China, but I think it has the some of the best prospects of surprising the market and flying higher over the next six months.

If you would like to find out which sector that is and want to know how I managed to jump on uranium and gold before the big gains occurred…I have a video series I want to give you.

I will explain the process I followed and discuss an ETF that I reckon could benefit if I’m right about the coming breakout.

More details on Friday.

Regards,

Murray Dawes, Editor Retirement Trader and Fat Tail Microcaps

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Berkshire Hathaway held its Annual General Meeting on the weekend. It began with a touching tribute to Charlie Munger, who passed away in November, aged 99. It’s well worth the watch. It starts around the 30 minute mark, here.

The meeting coincided with the release of Berkshire’s fourth-quarter report. It revealed the conglomerate now has around US$190 billion of cash and treasuries on its balance sheet, a record high.

Clearly, Warren doesn’t see a great deal of opportunities at these prices.

He also sold a good chunk of Apple stock during the three months to 31 March, reducing Berkshire’s stake by around 115 million shares, or 13%.

That means Apple still represents around 37% of Berkshire’s stock portfolio, so he’s hardly bailed on the position.

What doesn’t get much attention is Buffett’s exposure to traditional energy stocks. Chevron Corp and Occidental Petroleum are his fifth and sixth largest holdings, representing 9.6% of his listed stock portfolio (US$33.5 billion) at the end of 2023.

This is worth keeping in mind if you’ve drunk the renewables Kool-Aid in recent years and have little exposure to energy. Murray Dawes will have more on this for you in Wednesday’s Insider.

For today though, here’s an essay I wrote for Livewire last week. The short version is that when anything becomes too popular in markets, it’s at risk of not working.

My view is that ‘quality’ stocks are now so well-liked and understood that they pose a risk to investors. Investors are pricing their high rates of returns on capital as if they will go on indefinitely.

But as Buffett once said:

‘Truly great businesses, earning huge returns on tangible assets, can’t for any extended period reinvest a large portion of their earnings internally at high rates of return.’

Why investors in ‘quality’ are

headed for a fall

It seems everyone these days only wants to buy ‘quality’. Quality investments are all the rage. Which makes sense. Of course you should aim to have quality stocks in your portfolio.

But what a lot of investors are ignoring is the price they are paying for quality. Remember the Nifty50 bubble of the late 1960s and early 1970s? Everyone thought you couldn’t go wrong buying quality large-caps — stocks like IBM, Xerox, McDonald’s, American Express, and Eastman Kodak.

And while some of these worked out to be fine long-term investments, you would have had to have nerves of steel or complete ignorance to hold on.

In this wire, I’m going to explain why paying a high price for a quality stock will lead to mediocre long-term returns.

But first, a caveat…

If you’ve bought these companies at a fair price, sitting tight is the way to go. Thinking you can take some profits and buy back in when prices fall is a low-probability strategy. Plus, there are transaction costs and taxes to take into account.

So, if you’ve bought right, sit tight!

Now, let’s define what we mean by quality. I’m not sure there is an official definition, but I’d say it would be something like this:

‘A company that generates sustained high returns on tangible capital (thanks to a competitive moat) and compounds those returns via reinvestment.’

The US tech companies are the pin-up stocks here. They can compound at high rates of return for years because the US economy is massive, giving them a huge growth profile from start-up phase to national dominance. Then, national success often leads to global success, which offers another growth runway and compounding opportunities.

Google, Facebook and Amazon are good examples of this. And, of course, there is Apple, Netflix and Nvidia.

You also have companies like Visa and Mastercard that have huge network effects and ongoing growth prospects as society goes cashless. All these companies generate very high returns on tangible capital and significant free cashflows.

Chris Mackay’s MFF Capital Investments [ASX:MFF] is the best local exposure for quality global growth stocks. It’s one of the few investment funds that isn’t afflicted by what Buffett termed the ‘institutional imperative’. That is, bureaucracy over rationality.

His monthly commentaries are always good reading too. Take this snippet from early April:

‘Higher prices are riskier, not less, and presage lower future returns, not higher. Sentiment can change quickly, and will change eventually, as company/industry specific issues and geopolitics, elections, inflation/stagflation/interest rates assume fluctuating levels of importance for market participants, the vast majority of which are not investing in equity markets for long term exposure to sustainably advantaged businesses.’

That last bit is an important point for you to keep in mind. Although the ‘stock market’ and ‘investors’ are common word associations, you’d be wrong to believe it wholeheartedly.

The vast majority of activity on the stock market has nothing to do with investment. There’s an army of analysts, brokers, investment bankers and traders that must be fed. If everyone is an ‘investor’, meaning they buy, hold and wait, a lot of stock market participants will go hungry. Activity is the name of the game.

Don’t forget that when you’re scratching your head about share price movements. In the short-term, it is nearly all noise.

But Chris’ first comment is pertinent to this wire’s main topic: ‘Higher prices are riskier, not less, and presage lower future returns, not higher.’

That is, the higher the price you pay for a given level of earnings growth, the lower your future return will be. It doesn’t matter if the stock is a quality one or not.

Railroads and AI

I don’t know whether the big tech stocks are overvalued or not. I do know they are probably the most dominant companies in history in terms of their profitability and compounding opportunities.

The big risk factor in terms of their future value is the significant capital expenditure required to build an AI capability. What will the future sustainable returns be on this investment? Will it be like other revolutionary infrastructure, like the railroads and the internet, where excess capacity led to lower initial returns on investment?

Who will the benefits of AI accrue to? The users or the providers? The users, definitely. But will the providers overinvest to stay ahead of the game? That’s the risk.

If that’s the case, and the main players compound earnings at a lower rate into the future, their intrinsic value will decline.

I don’t have any special insights into how this will play out. The main point to realise is that intrinsic value is all about the sustainable return on invested capital a company produces (and the rate at which it reinvests that capital).

As far as the Aussie market goes, we have a lot of ‘quality’ companies…just not in the same league as the tech giants.

But they have certainly benefited from the market’s renewed fervour for quality compounders, thanks to the phenomenal growth of these globally dominant tech firms.

Aussie Quality Compounders

Let’s have a look at a few of them now and see what future long-term returns ‘investors’ can expect by buying at current prices.

Remember, by ‘quality’ we’re looking for companies with high returns on tangible capital, with preferably the opportunity to compound these returns through high levels of reinvestment.

But how do you estimate future long-term returns? Short of plugging growth estimates into a discounted cash flow model and working out the implied discount rate (which would be the expected return) there are a few rules of thumb.

The more well-known one is to invert the P/E ratio and turn it into an earnings yield. So a stock on a P/E of 20 trades on an earnings yield of 5% (1/20).

Another way to assess the earnings yield, and make comparisons across businesses easier, is to adjust for differences in debt and tax payments. You do this by using EBIT (earnings before interest and tax) as your earnings proxy and EV (enterprise value, which is a company’s market cap plus net debt minus available cash) as the price proxy.

The earnings yield of a company thus becomes EBIT/EV

Using this formula (and consensus estimates for FY25) here is a list of large and mid-cap ‘quality’ stocks and their earnings yields:

Wisetech — 1.8%

REA Group — 3.6%

Cochlear — 2.9%

Pro Medicus— 1.3%

Netwealth — 3.3%

Lovisa — 4.4%

PWR Holdings — 3.8%

Car Group — 4.2%

Wisetech is the standout here. Pre-tax operational earnings forecasts for FY25 represent an earnings yield of just 1.8%.

That’s ok…it’s a growth company!

Let’s assume pre-tax profits double. That gives an earnings yield of 3.6%. And if they double again, that takes it to 7.2%. But the ‘investor’ only receives earnings after the tax man has grabbed his share. So, after tax, you’re still only looking at an earnings yield of around 5%, and that’s after I’ve heroically assumed earnings growth of 4x from here.

You can get a term deposit for that with very little risk!

You can do similar maths with the other stocks on the list. And keep in mind it is no easy feat to double profits. For larger growth companies, it takes years to do so.

What’s good is bad

Yes, these companies are ‘quality growth’. But quality and growth have become so popular that they are now more a speculation on future share price growth rather than an investment based on traditional risk/reward characteristics.

In investing, what’s popular almost never works in the long-term. What feels good now will almost always feel bad in the future.

The message is simple, don’t pay any price for a company, even the good ones. Use basic rules of thumb (EBIT/EV) and common sense to understand what you’re really getting when you buy.

Based on my small sample above, a lot of investors are locking themselves into poor long-term returns by jumping on the ‘quality growth’ bandwagon.

***

What do you think? Are investors becoming complacent? Let me know at letters@fattail.com.au

Regards,

Greg Canavan, Editorial Director, The Insider

Yen Rescued from the Precipice

By Murray Dawes

In this Issue:

The week started with a bang as the Japanese yen got hammered to levels not seen for 25 years.

The Bank of Japan decided enough was enough and stepped in to support the yen.

In today’s Closing Bell video, I show you the explosive set-up in the USDJPY based on over 50 years of data.

There is easy money being made by ‘carry traders’ those borrowing cheaply in yen and investing the proceeds into US bonds at much higher rates.

As long as the yen behaves and continues to depreciate due to the large interest rate differential between the two nations, the trade is like shooting fish in a barrel.

However, problems can arise if huge currency volatility erupts, eating into returns.

If BOJ intervention causes the yen to strengthen more than investors expect there could be some unwinding of carry trades which could end up placing upward pressure on US bond yields at just the wrong time.

Alternatively, if the BOJ fails to stop the rot in the yen and we see the USDJPY busting above 160 there is the real chance the yen could see very sharp falls.

That would place immense pressure on the BOJ to start raising rates.

By the end of the week the USDJPY had fallen from 160 to 153 (meaning the yen strengthened) which is a large move.

The game of cat and mouse between market participants and the BOJ is now on. It bears watching because of the possible repercussions for global bond and stock markets if we see wild swings.

The other market that I zero in on today is copper, due to the sharp rally we have witnessed over the last month.

The copper price is nudging up against some serious resistance, but the big picture is now looking incredibly bullish.

Any weakness in copper prices over the next few months should be seen as a buying opportunity and I show you the level copper needs to fall below to negate my current bullish stance.

I finish off today by outlining the state of play in the S&P 500. There has been some weakness over the past month on the back of high inflation and weak bond markets, but the weekly and monthly trends remain up.

As I show you in the video, short-term momentum is negative, but I need to see the weekly trend turn down before I change my bullish stance on stocks.

Regards,

Murray Dawes,

Editor, Retirement Trader and Fat Tail Microcaps

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

In last week’s Insider I said I’m going to focus on THE most important thing to understand when it comes to investing. It’s more important than valuation, company analysis, or mastering the ‘technicals’.

It’s understanding investor psychology, and how your brain plays tricks on you.

Last week, we looked at how your brain works when it’s under the influence of ‘greed’. This week, let’s see what ‘fear’ chemicals do to your emotions and decision-making abilities…

Fear chemicals are really stress chemicals. There are two major ones that are relevant to investors:

Adrenaline, and

Cortisol.

Adrenaline is known as your ‘fight or flight’ hormone. It is produced by the adrenal glands immediately following a stressful situation.

For example, when you see the stock market plummet…or a key stock in your portfolio fall sharply (Bapcor, anyone?), that reaction you feel immediately is due to a surge of adrenaline. It’s in response to a threat to your financial survival.

The adrenaline gives you a surge of energy. This is why you have trouble sitting still or thinking calmly when you’re in this situation.

Cortisol is known as your ‘stress hormone’. It is also produced by the adrenal glands. Cortisol takes a little longer for your brain to release than adrenaline, which is immediate.

That’s because it is a multi-step process. The amygdala (the fear centre of your brain) recognises a threat and sends a message to your hypothalamus. It then sends a message to the pituitary gland, which in turns sends a message to the adrenal glands to produce cortisol. I don’t know why it’s a multi-stage process. But I’m not going to argue with a few billion years of evolution. I’m sure the brain has its reasons.

In effect, stressful situations, like stock market crashes or high levels of price volatility, result in the production of both adrenaline and cortisol.

The production of these chemicals is an evolutionary design to get you out of what has historically been a more pressing threat than a wobbly stock market.

Let’s have a look at the physical effects of an increase in stress hormones. Adrenaline increases the heart rate and engages the muscular and respiratory systems. Cortisol, on the other hand, increases glucose levels to the muscles, and temporarily inhibits other body systems, including the digestive, reproductive and immune systems.

This is why those suffering from ‘chronic stress’ — too much production of cortisol — suffer physically, because other important systems (for example, the digestive system or immune system) are on hold to fight the perceived threat.

These neurochemicals are crucial to our survival. We need them when driving a car, walking in an unfamiliar neighbourhood at night, or playing a high stakes sporting contest.

This is your fearful brain on stocks

But they’re not so great for us in the world of investing. Consider that your brain is the result of a few billion years of evolution, while stock markets have been around for only a few hundred years.

In other words, your brain isn’t at all well equipped to deal with stock market investing. And if you’re not aware of your brain’s susceptibility to it, you’ll make the same investing mistakes over and over again.

Your brain also stores fearful memories. This can then act as an inhibitor to you taking action when a genuine investment opportunity presents itself.

For example, when you go through a highly stressful investing experience, like what happened to most people in 2008, or in 2020, your amygdala fires up so intensely that it effectively leaves a scar…an indelible memory of the experience.

As Jason Zweig explains in Your Money and Your Brain:

‘Traumatic experiences activate genes in the amygdala, stimulating the production of proteins that strengthen the cells where memories are stored in several areas of the brain. A surge of signals from the amygdala can also trigger the release of adrenaline and other stress hormones, which have been found to “fuse” memories, making them more indelible. And an upsetting event can shock neurons in the amygdala into firing in synch for hours — even during sleep. (It is literally true that we can relive our financial losses in our nightmares). Brain scans have shown that when you are on a financial losing streak, each new loss heats up the hippocampus, the memory bank near the amygdala that helps store your experiences of fear and anxiety.

‘The amygdala seems to act like a branding iron that burns the memory of financial loss into your brain. That may help explain why a market crash, which makes stocks cheaper, also makes investors less willing to buy them for a long time to come.’

It makes sense, doesn’t it?

When the market falls, your brain interprets it in the same way it would a physical threat. It releases stress hormones to enable you to deal with the threat. But in a 2008 or 2020 type environment, where the market falls relentlessly, the stress of dealing with that becomes unbearable.

Your amygdala is so active and in control of your brain that it hijacks your cortex (your rational brain) completely.

This is why you often sell at or near the bottom. The strain is just too much and the only way of relieving the stress is to sell.

Once you sell, your amygdala calms down and your adrenal glands get a rest. This allows your cortex back into the conversation and by this time, the market may have bounced. Because the cortex is back in control, this is when you kick yourself for selling at the bottom. You feel stupid.

But if the experience was traumatic, like it was in 2008 or 2020, your amygdala has such vivid memories that it can override your rational brain for some time.

You know stocks are cheap. You know that buying when others are fearful is the ‘right’ thing to do. But your fear centre holds you back. It still thinks it’s unsafe. It’s worried about further falls.

It’s only when the fear starts to recede, often years later, that investors go back into the market.

This is why stock markets are a largely psychological phenomenon. They are as much about human emotions (driven by the limbic system) as they are about fundamental factors such as company earnings, economic growth and interest rates.

When you learn to look at the market as a highly complex living organism – driven in part by emotion and in part by fundamentals, you will ‘evolve’ into a higher-level investor.

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Conditions in bond and stock markets continue to point to a correction in asset prices dead ahead.

Commodities are the one bright spot, with copper continuing to spike higher which seems to be feeding into other metals such as zinc, lead, aluminium, and even the serial underperformer nickel.

After a blistering six month rally in the S&P 500 on the back of the Fed pivot last October, it feels like stocks are about to suffer a reality check as sticky inflation pushes rate cuts out further and further.

The US 10-year bond just confirmed a monthly sell signal based on my trading model. US 2-year bonds are back above 5% which must have a few highly indebted companies due to rollover debt in the next few years squirming in their seat.

The euphoria created by the Fed last October combined with the AI frenzy has taken US stocks to a P/E near 21, which is looking stretched.

I’ve been amazed by the strength in US stocks over the last four months as US 10-year bond yields jumped from 3.8% to 4.7%.

But I think the period of ignoring the worsening inflation numbers and sell-off in bonds is over.

There has been a large spike in passive investing over the last few years. Interest in ETFs (Exchange Traded Funds) is soaring.

Passive investment just allocates money to stocks based on their membership and weight in an index. If BHP Group [ASX:BHP] is 10% of the index then 10% of the money coming into the fund goes into BHP.

I’m sure you can appreciate that the higher the amount of passive money going into the market, the higher the odds are that a strong trend can continue beyond what you would expect.

Momentum traders also jump on strongly trending stocks and buy them for the simple reason that they are going up.

Perhaps the strength of the rally in US stocks over the past six months is a result of upside momentum leading to more upside momentum.

If that is the case there will come a time when the music will stop, and the strong uptrend will shift to a strong downtrend in the blink of an eye.

Everything hinges on the future path of inflation and interest rates.

US services inflation is currently running at an annualised pace of around 6–7%. That is too high to ignore and must come down rapidly if CPI has a hope of gravitating back towards 2%.

Unemployment remains very low, and wages growth is running at 4.4%.

Australia is in a similar position, but our interest rate setting is far less restrictive than the US.

We usually have interest rates set about 1–1.5% above US interest rates.

Currently our interest rate setting is at 4.35%, which is nearly 1% below US rates.

I reckon the RBA is dead scared of toppling the housing market if they raise rates too far. But that reticence could force them to raise rates higher down the track if inflation continues to fester.

Perhaps the shift towards hard assets that we are witnessing in commodity markets is another red flag that inflation is still not under control.

Gold has already spiked dramatically over the last few months and is at risk of a correction as real rates start heading higher again.

But I think you would be a buyer of gold and gold stocks if we saw a fall to around $2,100.

The sharp rise in copper is the thing that has tongues wagging and I’ve noticed strong buying recently in the other commodities mentioned above.

So despite the fact US stocks are looking top heavy and weak bond markets could ignite further selling, Australia may be well placed to ride another bull market in commodities.

Investors should be eyeing off their portfolio and considering how interest rate sensitive it is, now that the hope that inflation would drop like a stone is fading fast.

The other bit of news that I think is worth keeping an eye on at the moment is the sharp fall in the Japanese Yen.

As US rates march higher there is rising tension in the Yen while the BOJ keeps rates near zero.

The USDJPY has hit levels not seen since 1990 after breaking out of a long-term range.

The BOJ intervened the other day to support the yen, but I doubt they will be able to stop the rot and may even cause further selling.

If the yen continues to nosedive there will be immense pressure on the BOJ to start raising rates. Inflation in Japan has dropped from over 4% at the start of 2023 to its current level of 2.7%.

A large plunge in the yen could see inflation shooting higher again.

Perhaps the only outcome from a plunging yen is that we should all go for a holiday in Japan soon, but if the yen plunges dramatically it may have knock on effects to other markets.

The carry trade involves borrowing in yen at low cost and investing the proceeds into say, US government bonds at a much higher yield. That will be providing much needed buying support in US bonds at a time when buyers are scarce.

An imploding yen which leads to higher Japanese rates may see an unwinding of carry trades, for example, which could cause US rates to rise.

I’m not saying that as a prediction. Just pointing out that dramatic moves in major currencies can often be a canary in the coal mine prior to major market dislocation events, so it’s worth keeping an eye on the yen to see if the sell-off becomes disorderly.

Regards,

Murray Dawes, Editor Retirement Trader and Fat Tail Microcaps

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

I read an article in the Financial Review last week that tells you everything you need to know about where we are in terms of societal and monetary degradation.

I’d never heard of Larence Escalante before. But according to the Fin, at age 42, he’s one of the county’s youngest billionaires with an estimated wealth of $3.2 billion.

Did he cure cancer? Have a hand in the AI revolution? Invent an indispensable widget?

No, he is the founder of Virtual Gaming Worlds, operator of the apparently ‘wildly successful’ Chumba Casino…whatever that is.

Here’s a bit of an insight into this upstanding citizen:

‘When he’s not flying around on a Bombardier 7500 emblazoned with his nickname Lee – funded with a multimillion-dollar loan from retailing billionaire Gerry Harvey – he’s riding around in a supercar or importing Lamborghini yachts. Lingerie-clad waitresses pour Dom Pérignon at a private club in his hometown, Perth. In Hong Kong, he’s on a shopping spree for rare Rolexes.

‘He’s living so large that he escaped a conviction in Victoria late last year for bringing small amounts of drugs into Australia on the way back from Las Vegas. He had been “partying with literally 20 friends,” and “didn’t even know he had it,” as he told Australian Border Force officers at the time.’

I usually don’t like to have a crack at people like this. He can spend his money however he wants. But it’s an insight that is important. It tells you this is an easy come, easy go wealth.

And it’s the easy come bit that gets under my skin. Because governments are deliberately fostering it with their spendthrift ways.

As the article makes clear, even if it doesn’t say so specifically:

‘But it was the COVID-19 pandemic that was transformational for the company. It recorded net profit of $115.8 million in the six months to the end of December 2020, a 60 per cent increase on the 2019-20 financial year.

‘“Covid turbocharged the business and in 2021-22 Laurence became very wealthy,” Reichel, Virtual Gaming Worlds’ former chief operating officer, tells The Australian Financial Review.’

Let’s be clear. COVID-19 the virus did not make people suddenly want to gamble. It was governments response around the Western world that shoved money into people’s pockets, while forcing them to stay at home, that created this God-awful boom. Easy come, easy go.

That’s why we have a persistent inflation problem. It’s not because monetary policy isn’t tight enough. It’s because fiscal policy is too loose. It’s not just the quantum of spending. It’s the type of spending.

Billions going into NDIS which is encouraging thousands to game the system. Billions going into renewable energy with the result being higher energy prices.

Before COVID there were just over two million public sector employees, with a total wages bill in 2019/20 of $174 billion.

In June 2023 there were 2.43 million public sector employees with a 2022/23 wages bill of $215 billion.

That’s a 21.5% increase in employees and a 23.5% increase in wages.

In the US, Jason Zweig at the Wall Street Journal writes:

‘Since the first quarter of 2020, the total public debt of the U.S. has risen from $23.22 trillion to more than $34.5 trillion—with almost $400 billion expected to be issued next month alone.’

That’s a US$11 trillion increase in government debt and spending in four years! How much of that spending is about creating demand rather than supply? The inflation figures give you the answer.

The politicians can put on show trials with supermarket execs price gouging all they want. Some people will fall for it. But the source of inflation is government itself. It always has been and always will be.

And when you create too much money and hand it out to buy popularity, it creates an easy come, easy go mentality. People start to punt…on stocks, in casinos, online…wherever. And that easy money ends up in the pockets of people like Mr Escalante. And from there, the easy money goes to all sorts of ‘luxury brands’, as you can see below.

It shouldn’t come as a surprise to see that the Roundhill S&P Global Luxury ETF (ticker code LUXX) hit the boards at the back end of the boom in August 2023. It’s gone sideways since.

Again, if blowing your money on a Lambo yacht or a branded handbag is your thing, go for it.

But if you have respect for your hard-earned and want to protect it from the idiocy of government destruction, buy gold (or Bitcoin if you don’t need 5,000 years of history on your side).

If you want more bang for your buck, buy gold stocks over gold bullion. But be aware of the risks that come with that.

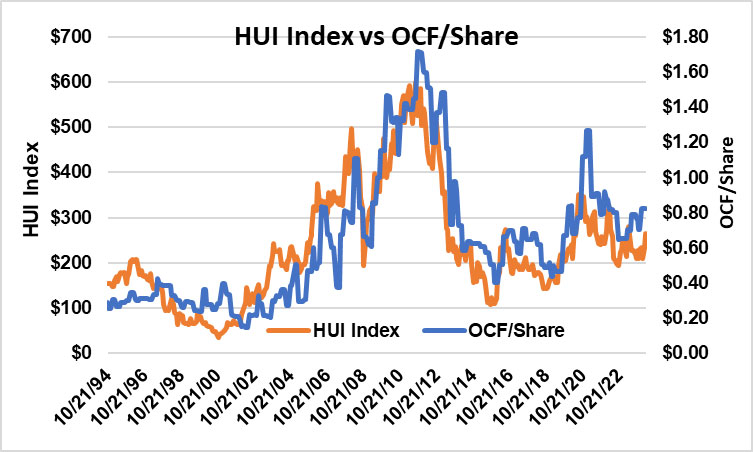

I read a great thread on X last week (@GarrettGoggin) that explained why the major gold stock index (the HUI index) was down 50% since 2011, despite the higher gold price.

It comes down to the huge issuance of shares that have obviously diluted returns. The chart below tracks the index against operating cash flow per share of the big players – Newmont, Barrick, Agnico and Kinross.

Operating cashflow per share is lower now than what it was back in the previous bull market. Inflation (along with a gold price that went nowhere for more than a decade) decimated margins and earnings.

This put pressure on companies to raise capital (and issue new shares) to fund expansion.

But the gold price is now at a level where good companies generate enough capital to self-fund their expansion. So excessive share issuance should become less of a problem going forward.

That should provide a boost for gold stocks in the years ahead as the cycle turns.

If you’re interested in finding out about some of the best speculative gold stocks on the ASX, you have until tomorrow to check out Brian Chu’s latest presentation.

After a strong finish to last year in the ASX 200, 2024 started off on the right foot with a breakout above the previous all-time high hit in August 2021.

US stocks were powering ahead day after day and the Aussie market went along for the ride, with small caps also coming back to life after a couple of horrible years.

It may surprise you to know that the ASX 200 is currently trading at 7,590, which is exactly the same level it closed at on the final trading day of 2023.

In other words, the last four months trading has gone nowhere fast.

The reversal of fortunes in the bond market is the culprit, with the goldilocks scenario of falling inflation and interest rates combined with resilient growth starting to look like wishful thinking.

I have been alerting you to the weakness in US bonds for a while, preparing you for the possibility that stocks would soon encounter selling pressure if rates kept rising.

US GDP figures released on Thursday showed growth slowing rapidly and inflation remaining elevated.

GDP for the first quarter came in at 1.6% which was well below expectations of 2.5% growth. The Core PCE deflator (one of the Feds preferred measures of inflation) hit 3.70%, well above expectations of 3.40%.

Slowing growth and rising inflation is never what you want to see.

In response, US 2-year bond yields closed above 5% for the first time since November 2023 and US 10-year bond yields headed above 4.70%.

US stocks were weak for most of the day but turned higher on the back of solid results from Alphabet (Google) [NASDAQ:GOOGL].

With only a few days left in April, it looks like we will see a monthly sell signal in US 10-year bonds confirmed. The long-term trend in yields remains up, so investors should be aware that further weakness in bonds should be expected.

Greg Canavan and I have already taken evasive action, exiting interest rate sensitive stocks in our services over the past few weeks.

As I show you in the Closing Bell video above, the long-term trend in US and Australian stocks remains up, but weekly momentum has turned negative.

It is a situation that calls for some caution, but certainly no need to panic. Investors who have enjoyed the run over the past six months may consider taking a bit of money off the table, but positioning should remain long until further proof of a larger correction is confirmed.

In today’s Closing Bell, I look at previous economic cycles and the path of two-year interest rates so you can understand the current state of play.

Regards,

Murray Dawes,

Editor, Retirement Trader and Fat Tail Microcaps

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Over the next few weeks, I’m going to focus on THE most important thing to understand when it comes to investing. It’s more important than valuation, company analysis, or mastering the ‘technicals’.

It’s understanding investor psychology, and how your brain plays tricks on you.

Charlie Munger was famous for his multidisciplinary approach to investing. He put understanding psychology up there as one of the most important disciplines for an investor to master.

He was so impressed with the book Persuasion, that he gifted the author, psychologist Robert Cialdini, a share of Berkshire Hathaway.

What I want to do over the next few weeks is give you an understanding of just why your brains works in the way it does in certain circumstances. If you understand the mechanics of the brain when it comes to dealing with investment markets, you might be better able to control its impulses.

Buffett and Munger have long said that they are not particularly intelligent. Rather, they just practice the right temperament for investing.

I would argue that they are very intelligent. But this isn’t their edge. Many intelligent people fail in investing. Their edge is their temperament. They have mastered their emotions.

I’m not saying you can do it too. It’s obviously hard. But understanding how your ‘software’ system works is a good start on the road to being able to program it better.

The simple fact is that the brain has not evolved to deal with investment markets. That’s why so many investors lose when they first start out. Not because they picked the wrong stocks, but because they succumbed to emotional pressures. These pressures are the result of our innate software program that runs in the background.

What is this program?

At a very basic level, I guess you’d call it a survival program. By that I mean social survival. We can’t survive on our own. We need to cooperate to ensure we have adequate shelter, food and water, and clothing. We are, therefore, social creatures. And evolution has ensured we are rewarded for social behaviour.

How?

Our brain releases neurochemicals to reward behaviour that promotes survival. It also releases other neurochemicals to discourage behaviour that threatens our survival (physical or social).

In her book, I, Mammal, Dr Loretta Breuning writes:

‘Humans have a big cortex and a big capacity to learn from experience. But we cannot short circuit our mammalian limbic system. Our cortex gives our limbic system information to make better decisions, but our limbic system still controls the neurochemicals that link mind and body. Our actions ultimately come from our neurochemical selves.’

Fear and greed chemicals

What are these neurochemicals? Let’s call them:

1. Fear (or stress) chemicals, and

2. Greed (or happy) chemicals.

From an investment perspective, these are the chemicals your brain releases (via the limbic system) at extreme highs or lows in individual stocks, or the stock market as a whole. These chemicals override your rational brain and make you do things you later regret.

They make you buy at the top and sell at the bottom. Which is really annoying.

Knowing what these chemicals are, how they work and why, will give your rational brain — your cortex — the best opportunity to override the evolutionary survival impulses fired off by these neurochemicals.

Given that we’ve been in a ‘greed’ phase for the past few months, let’s take a look at how these chemicals work to influence our behaviour. Next week, we’ll examine the effect of fear chemicals.

The greed chemicals are:

Dopamine

Serotonin

Oxytocin

Dopamine: The offer of a big reward

Dopamine is the big one here. Previously, researchers believed that the brain produced dopamine in response to obtaining a reward. Now, it’s thought that dopamine comes from the expectation of a reward. It’s a motivating chemical.

Consider how Dr Loretta Breuning puts it in her book, Habits of a Happy Brain:

‘Our ancestors didn’t know where their next meal was coming from. They constantly scanned their surroundings for something that looked good, and then invested energy in pursuit. Dopamine is at the core of this process. In today’s world, you don’t need to forage for food. But dopamine makes you feel good when you scan your world, find evidence of something that felt good before, and go for it. You are constantly deciding what is worth your effort and when it’s better to conserve your effort. Your dopamine circuits guide that decision.’

Translated to the game of investing, this is what happens in a bull market when you’re planning to buy a stock. You might have already made some gains on a particular stock. If you see a similar situation unfolding in another stock, its potential excites you. That’s the dopamine flowing. It provides the motivation for you to take the risk and place the trade. Motivation = decision = action.

Dopamine especially flows when the reward you get exceeds your expectation. Say you buy a stock expecting steady price appreciation. But a takeover announcement sees it soar 50% instead. At that point, you get a surge of dopamine as a reward and motivation to do it again.

Unfortunately, unexpected rewards are hard to replicate. That’s why they’re unexpected. The craving for dopamine leads you to take increased risks to try and obtain your past investment high. Such a pursuit generally leads to trouble.

I think this is partially why winning streaks typically end in tears. In your attempt to replicate past successes, you often take on riskier bets and replace sound judgement with hope. That never works well.

Dopamine has us constantly searching for the next big winner. That’s why people love punting on tiny resource stocks, cryptocurrencies, or tech stocks. The offer of a big reward gives us a dopamine high.

While this is fine if it’s controlled, keep in mind that dangerous habits can form, especially if you’re ‘unlucky’ enough to stumble on some early winners.

Early (and unexpected) winners give you the dopamine rush that you continue to seek out. It can turn into a form of addiction. Consider the following, from Jason Zweig’s, Your Money and Your Brain:

‘At Harvard Medical School, neuroscientist Hans Breiter has compared activity in the brains of cocaine addicts who are expecting to get a fix and people who are expecting to make a profitable financial gamble. The similarity isn’t just striking; it’s chilling. Lay an MRI brain scan of a cocaine addict next to one of somebody who thinks he’s about to make money, and the patterns of neurons firing in the two images are “virtually right on top of each other”, says Breiter.’

That’s why making easy money when you first start out is dangerous. Through the release of brain chemicals, you’re conditioned to think this is the norm. So you continue to chase the feeling by taking bigger and riskier punts.

Serotonin: A swarm of locusts

Serotonin explains why we get sucked into investment fads. It’s another survival-promoting chemical found present in every living thing.

In the animal world, serotonin is released when access to food is secure.

Animals also enjoy a serotonin release when they rank higher in social status. This provides a clue as to how it works with humans and investing.

Dr Loretta Breuning gives a few examples in her book, I, Mammal:

‘In an experiment with an alpha male vervet monkey and his subordinates, researchers placed a one-way mirror between them. The alpha male could see his troop, but they couldn’t see him. During his displays of dominance, the troop didn’t react with its usual deference. After several days of this, the alpha male’s serotonin levels dropped, and his anxiety levels increased.’

Doing better than others in the investment game? Enjoy that sweet flow of serotonin…

And then there is this interesting finding between serotonin and locusts.

‘Serotonin has been found to play a curious role in the behaviour of locusts. A locust generally avoids other locusts, but serotonin transforms them into swarm creatures. Locusts produce serotonin when they get jostled and stimulated by fellow locusts due to overcrowding. Once their serotonin is triggered, they seek each other out, creating a pestilent swarm in pursuit of food. Serotonin makes them sociable when solitary food seeking cannot satisfy their needs.’

It is easy to see the similarities here between swarming locusts and investors (or speculators) swarming around the latest investment fad. Being part of a crowd searching for food (or big returns) makes people feel good. Serotonin is the feel-good chemical.

Because we have evolved to crave this chemical, being part of a crowd feels good. And when you’re invested in a stock or asset class that is doing well, you feel good when you tell others about it. It elevates your social status, if only in your eyes, and if only for a brief time.

Oxytocin: The comfort of crowds

Oxytocin performs a similar, if slightly different, role. It’s the chemical release we get from the comfort of crowds. For example, when a sheep can’t see another member of the flock, it panics and its brain releases cortisol. But when it joins the flock again, the brain produces oxytocin.

Humans (and most types of mammal species) are stronger in groups or herds. That’s why we’ve evolved to live in ever larger groups — it promotes survival. Oxytocin is the neurochemical that provides the feel-good factor to promote this survival.

When you’re invested in an asset class that is flying, you get a buzz about being involved in a ‘community’ of like-minded investors. They’re like you and you’re like them.

You feel good when others agree with you, and you feel good when you read things that you already agree with. It’s why confirmation bias (filtering for information that confirms your existing beliefs) is so pervasive in investment markets. It’s the oxytocin!

Stock exchanges form, bubbles follow

There is evidence that trading in financial instruments took place in the early Italian republics of Florence, Venice and Genoa from the 1300s. However, this didn’t result in the establishment of formal stock exchanges.

The Dutch East India Company formed the first modern stock exchange in Amsterdam in 1602. The aim was to create a place where shares in the company could be traded in a secure and organised manner.

Perhaps not coincidentally, one of the first recorded speculative bubbles took place in the Netherlands, or the United Provinces as it was called at the time, soon after the Amsterdam exchange started operating.

The tulip bubble, or tulip mania as it came to be known, gripped the Dutch population in 1636-37. There were clearly a lot of happy chemicals floating around at the time.

Less than a century later, the South Sea Bubble of 1720 inflated in London. Thousands of speculators joined in, but it was a short-lived party. The bubble soon burst, ruining thousands.

This bubble episode is the source of the well-known quote from Sir Isaac Newton: ‘I can calculate the movement of the stars, but not the madness of men.’

It is not definitively known whether Newton lost money in the bubble or not. He was Master of the Royal Mint at the time and was influential in money matters.

So the quote may be a personal lament, or a response to a question of how far prices can rise.

Whatever the case, the point I’m making is that soon after large-scale trading of financial instruments began, people started succumbing to their emotions.

These emotions evolved over millions of years. They are designed to promote survival in a very different environment to the one that exists in the modern investment world.

In fact, survival in the investment world rewards behaviours that go against our evolutionary instincts!

If you want to be a better investor, then, you have to think and act differently from the investment herd. But being with the herd generates feel-good neurochemicals. That’s why it’s not easy to break away. When you do, you feel vulnerable and threatened. The stress hormones adrenaline and cortisol rise in response to ‘being alone’.

It’s why being bearish in the midst of a bull market or bullish in the depths of a bear market is often described as a ‘lonely’ place to be. It doesn’t feel good.

Even though the rational part of your brain knows that it’s the right place to be, your mammal brain makes it exceedingly difficult for you to occupy this space. It simply goes against your evolutionary wiring.

Next week, I’ll look at how the fear chemicals work their magic on you and make you sell at the low…but only if you let them.

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

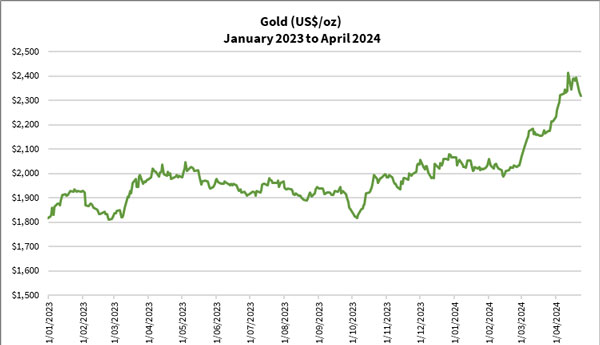

After trading in a tight range in 2023, it started 2024 poised to break out of its all-time highs of US$2,130 an ounce.

However, rather than follow the momentum from last October, it spent almost three months trading in a tight range, refusing to budge.

Things only changed in mid-March with the Federal Reserve Open Market Committee announcing that it was expecting three rate cuts this year.

Then gold took off.

Add to that the stoush between Israel and Iran two weeks ago that left the world pondering if there’d be a new military conflict.

Gold made a new record last Friday at around US$2,430 an ounce (more than AU$3,700) for two hours as Israeli missiles landed in Iran. Rumours swirled that they were targeting Iranian nuclear facilities.

The world held its breath.

Fortunately, the Iranian government came out to declare that there was little or no damage to key Iranian targets. And the government stated it won’t respond to the attack.

The world breathed a collective sigh of relief.

Gold did the same.

In the last two days, gold sold down as much as US$120 to US$2,300 as you can see below:

As gold threatened to fall below US$2,300, it looked as if the bullish narrative for gold was falling apart.

Focus on de-dollarisation, all else is a supporting act

Most of you are aware that I focus on the long-term when I evaluate the market and make my investment decisions.

That doesn’t mean I ignore the daily price movements. It can affect my emotions, as I’m human.

However, I try not to lose sight of the big picture.

In yesterday’s Fat Tail Dailyarticle, I wrote about how it’s important to focus on what drives the price of gold in the long-term.

It’s the US long-term real yield, which reflects the strength of the US dollar. The dollar pays interest to its holder, with inflation acting as a counter by diminishing its purchasing power.

Most people believe wars and major disasters drive gold’s rally. But the bulk of gold’s gains in the last 25 years came during times of relative stability.

Gold made steady gains as the central banks lent copious amounts of currencies to governments racking up deficits and stoking inflation.

Wars came and went. Some conflicts lingered on. However, the biggest driver for gold’s gains is the growing debt pile that threatens to discount global currencies into oblivion.

And until there’s a cure for society weaning off its reliance on government to solve its problems by creating more of it, you’ll see this cycle continue.

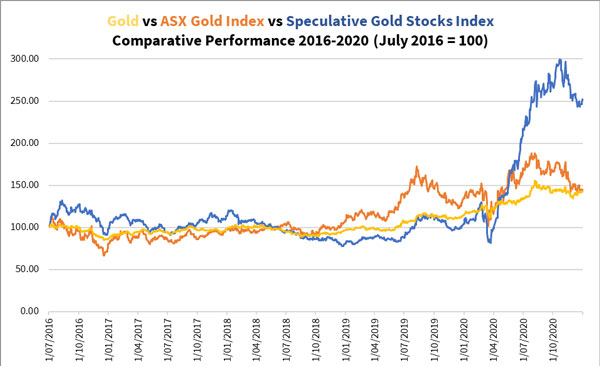

Gold stocks — Neglected, undervalued and poised for a major boom

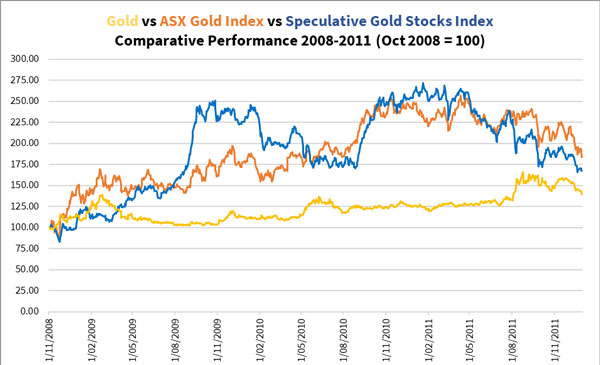

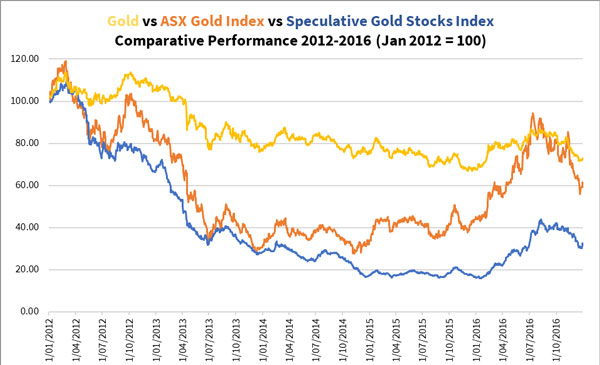

In the past gold bull markets, gold stocks either led or followed gold closely.

Have a look at the relative performance of gold, established gold producers (reflected by the ASX Gold Index [ASX:XGD]) and gold explorers (reflected by my in-house Speculative Gold Stocks Index) in 2009–11, 2015–16 and 2019–20:

In the 2009–11 boom, gold explorers jumped out of the gates and gold producers followed gold to make record highs.

The 2015–16 boom saw the reverse. Gold producers made astronomical gains while gold explorers staged an underwhelming rally.

The 2019–20 boom delivered strong gains for producers in 2019, only to have the gold explorers dwarf these gains when it staged a phenomenal rally in six months from March to September 2020.

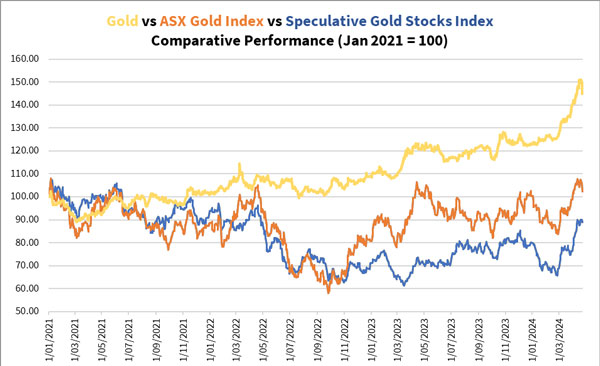

The last three years haven’t been the same.

And you’d expect that since the past doesn’t repeat. It does rhyme, however.

Gold rose steadily during the last three years, experiencing a lull in 2022 before trending higher into 2023.

It’s gone parabolic in the past month.

Meanwhile, gold producers and explorers have had a rough ride.

Even now, both are significantly undervalued compared to gold. Historically, they would be trading 50–150% higher.

And these are only the indices.

Individual companies should mint millionaires already, and I’m not exaggerating!

Take your positions now for a golden opportunity

The good news is that some companies are poised to turn thousands of dollars into much more.

Of course, there are no guarantees here that this will continue, but…

…to be specific, I’ve seen a few recover over 1,000% from their recent lows. It’s only been a few months since they bottomed too.

You’re not going to see it looking at these charts alone.

And I don’t encourage you to pick out companies trading at a few cents, or even less than 1 cent either.

There’re reasons why some companies trade at such low prices. They don’t have a story to attract the buyers and keep them.

Companies that can turn your life around must have quality projects, a sound plan, the right talents in the management team and a healthy cash balance.

Finding these companies take time. And you have to rely on some element of luck as there’s a lot of uncertainty in this space.

Not only that, you need to adopt the right strategy and mindset. Gold explorers are risky and highly volatile investments, and they can shake the undiscerning and impatient investor.

Success comes to those who can endure the challenge and ride through the thick and thin.

Members of my premium speculative newsletter, Gold Stock Pro, have endured a wild ride these three years. They’ve done the hard yards building their portfolio and holding on.

We’re ready to harvest our gains in the coming bull run.

Gold explorers are poised now to make a major run, as things are now falling into place for them.

Later this week, we’re re-launching Gold Strike 2024, allowing you a chance to build up a portfolio of gold explorers and early-stage developers to benefit from this gold bull run.

Why not consider joining us now for the potential to find life-changing opportunities?

God bless,

Brian Chu,

For The Insider

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Last week saw the long awaited correction in tech stocks. Nvidia fell 13.6%, Netflix 11%, Apple 6.5%, Amazon 6.2%, Meta 6%, Microsoft 5.4%, while Alphabet was down just 2.2%.

Given how far this sector has rallied since the October lows, this is not at all surprising, and I wouldn’t read too much into it.

Any opinion on last week’s tech stock performance will simply tell you more about the bias of the person giving it than anything else.

One move that did catch my eye was the Semiconductor index (the SOX) down 9% for the week.

The catalyst was some cautious commentary last week from the largest chipmaker in the world, The Taiwan Semiconductor Manufacturing Company (TSMC).

Although you wouldn’t know it from this Bloomberg article that the Australian Financial Review ran with last Thursday. The author, Jane Lanhee Lee, wrote:

‘Taiwan Semiconductor Manufacturing Co. expects revenue to rise as much as about 30 per cent this quarter, reflecting a boom in AI development that’s boosting demand for the advanced chips it makes for the likes of Nvidia Corp.

‘The better-than-projected outlook follows its first profit rise in a year, after strong AI demand revived growth at the world’s biggest contract chipmaker.’

But Jane must have seen the share price reaction and re-wrote the article. The Fin Review didn’t get the updated memo. Here’s how the new and improved version looked in Bloomberg news:

‘Taiwan Semiconductor Manufacturing Coscaled back its outlook for a chip market expansion, cautioning that the smartphone and personal-computing markets remain weak.

‘The world’s largest maker of advanced chips cut its expectations for 2024 semiconductor market growth — excluding memory chips — to about 10%, from above that figure. Chief Executive Officer C. C. Wei also trimmed his growth forecast for the foundry sector, which TSMC leads. Meanwhile, the company maintained its estimates for spending at anywhere between $28 billion and $32 billion amid capacity expansion and upgrades this year.’

Always remember, markets make opinions.

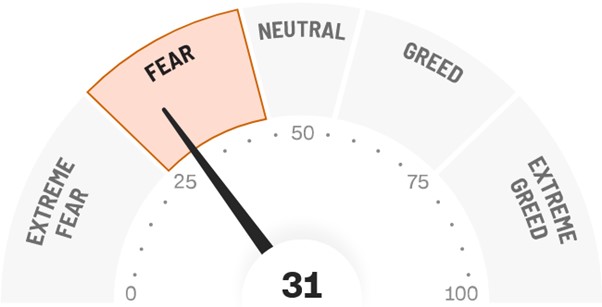

While I wouldn’t rely on the mainstream business media to tell you what’s going on, I do take note of investor sentiment. And it’s pleasing to see the CNN Fear and Greed index has fallen into a fear reading for the first time since October last year. In fact, it’s not too far off an extreme fear reading.

I say ‘pleasing’ because when the market is fearful prices tend to be more attractive. At the very least it means a bounce may not be far off. (You’ve seen that play out today.)

One thing I’m not seeing though is a lot of ‘value’ coming back into the market. Which makes sense, the ASX200 for example, is only down 4.4% from the peak. It’s hardly anything for value investors to get excited about.

I for one am hoping this correction will continue to unfold for the next few months and reveal some good value opportunities.

Veteran fund manager on what comes next

Callum Newman, who heads up the Australian Small-Cap Investigator and Small-Cap Systems services, had a chat with veteran fund manager Matthew Kidman last week.

As he wrote to his members:

‘I chatted with fund manager Matthew Kidman last week. We’ll have that full video up for your soon.

‘I mention it because Matthew flagged a possible sell down about now. Believe it or not, he said it would be “good” for the market.

‘It’s been a big run up in the market since November. Now we’re due a bit of a retrace. There’s nothing abnormal about it. Shares are volatile. Get used to it.

‘The main thing is to keep your eye on the big picture.

‘Bull markets don’t go up in a straight line.’

That interview is now up on Youtube. I highly recommend giving it a watch.

The relationship between oil and the market

I sent the excerpt below to members two weeks ago. I think it is something to think about in the months ahead. Not many people realise the liquidity sapping effects of a sharp rise in oil prices…

‘Brent crude is up 10% over the past month, and 25% since its December low. Like gold, oil looks due for a short-term pullback, but it looks to be building momentum for a move above US$100/bbl.

‘If that happens, the broad market rally you’ve seen over the past six months is at risk.

‘Why?

‘A rising oil price soaks up market liquidity. Oil is one of the largest markets in the world. A price rise of 25% means the oil market absorbs 25% more dollars.

‘The more the oil price rises, the more liquidity it soaks up. It’s got to come from somewhere, and that somewhere is ‘the market’.

‘The last major oil price spike occurred from March-June 2022. That wasn’t a good time for equity markets.

‘Back in July 2008, the oil price spiked to over US$140/bbl. A few months later, all hell broke loose. Oil wasn’t the cause of the GFC. But the rising price soaked up whatever liquidity was left.

‘Probably the most extreme example of this occurred back in the early 1970s with the Arab oil embargo quadrupling the oil price. The result was one of the most severe bear markets in history, the 1973/74 bear market.

‘I’m not suggesting that is on the cards here. I’m just pointing out that an oil price spike is not good for markets.

‘And it’s certainly not good for a market that has spent the past six months rallying on the belief that the Fed is about to pivot and cut rates. If oil continues its rally, which looks likely in the months ahead, rate cuts are off the table.

‘The US 10-year bond yield is already trading at 4.43%, up 34 basis points over the past month. The last time yields were at this level was back in November, on the way down. Back then, the S&P500 was about 15% lower.

‘Now, yields are on their way back up (along with oil) yet the market is completely ignoring it.

‘I don’t think you should.’

Well, last week the market decided to take notice of the jump in yields. A correction is now underway. How far will it go? Who knows. But I think the oil price will have a lot to do with the answer.

Markets have entered classic risk-off territory after news came out about the Israeli attack on Iran.

I write this on Friday afternoon so you will know more than me about what is going on by the time you read this.

Early reports are pointing to an attack on the Iranian nuclear program as well as an attack on a meeting in Iraq between various Iranian backed groups and the IRGC (Islamic Revolutionary Guard Corps).

This increases the risk that things could spiral out of control, so it is no wonder Mr market is running for cover.

Oil, bonds and gold are rallying, and stocks are falling.

Making predictions about the future path of geopolitical events like this is a fool’s errand.

The highest probability is that things will settle down again after a period of volatility.

The technical situation in US stocks was ripe for a correction so this news could be a catalyst that sets off some stop losses and leads to a sharp fall.

In today’s Closing Bell video I show you the target where I think the S&P 500 is heading to in the short-term.

I then give you a few different scenarios to consider.

Gold is flying higher on the news and should remain well supported while the situation remains volatile, but after such a strong run we should be prepared for a sharp correction if things settle down.

The oil price will let us know how seriously the world takes the current tit-for-tat going on between Israel and Iran. As I have been saying, if Brent crude oil heads above US$96 a barrel I have a target above US$110. This would cause some problems for stocks as they become worried about sticky inflation.

Click on the picture above to check out my latest Closing Bell video where I analyse the S&P 500, US bonds, gold, and the ASX 200 now that the correction is gathering steam.

Regards,

Murray Dawes,

Editor, Retirement Trader and Fat Tail Microcaps

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Before we get started, just a reminder that you have until midnight tonight to watch Ryan Dinse’s 4th Halving Gameplan presentation.

Tomorrow marks the 4th halving, after which, according to Ryan, the next crypto cycle begins.

The previous three cycles saw Bitcoin and many other cryptocurrencies reach all-time highs in the months following.

This time, we have institutional buying power coming into the market via the newly created ETFs. Bitcoin has already hit a new all-time high this year, a sign that Ryan says makes this halving event more bullish than ever.

We’ll see how it plays out, but for exactly HOW to play it – in the right way and in the right crypto projects – there’s no one better to help you than Ryan.

If you want in, you have to do so now – click here!

Now, let’s get stuck in…

***

In this week’s edition of Uncommon Sense Investing, I’m going to talk about the ‘equity risk premium’ (ERP) and what it means for you as an investor.

It sounds fancy, but it simply refers to the additional return equity investors seek above the risk-free rate to compensate them for investing in a company’s equity.

What, quantitatively, is the equity risk premium?

No one really knows. Academics and market players have been debating it for decades and no one is any the wiser.

The reality is that when sentiment is bullish and prices are high, the ERP is low. That is, you’re not getting adequately compensated for risk. And when sentiment is depressed and prices are low, the ERP is higher.

This is just another way of saying that risk is actually low when it feels high, and it’s high when it feels low. This is how the market works.

That’s why using an ‘adequate’ ERP is useful. It helps you recognise when actual risk is high or low via the opportunities that present themselves (or don’t) in these environments.

What is an ‘adequate’ ERP then?

I usually start with a discount rate (or required rate of return) of 8% for large, established companies. That represents a current equity risk premium of 3.65%. Whether that is adequate or not, I don’t really know. But I have found it to be a good starting point.

Before continuing, let me just go back to Part VII in this series. In it, I wrote about the crucial relationship between the price-to-book (P/B) multiple and return on equity (ROE).

Book value and shareholder equity are the same thing. So, the return you get on that equity will determine the price someone is willing to pay for it.

The higher the return, the higher the price.

Or, the higher the ROE, the higher the P/B.

If you only look at the P/B as a way to assess value, you’ll be led astray. You have to look at it in relation to ROE.

At the end of the last essay, I wrote the following:

‘You can test this out this relationship between ROE and P/B on any company you’re interested in. Just divide the ROE by the Aussie 10-year bond yield and the result will probably be in the vicinity of the current P/B.’

I apologise. I gave you a bit of a bum steer.

To be more accurate, you need to add the ERP to the 10-year bond yield. This is where I get the 8% from.

In the investment world, not many do this to be honest. They employ all sorts of wild strategies that seek to get a short-term edge. Remember when high-frequency trading was all the rage? That was 10 years ago. You don’t hear about it anymore.

Sticking to basic principles will work in the long term. And making sure you’re adequately compensated for investing in the stock market is a pretty basic principle. It’s so basic, that most people have forgotten about it or never learnt it in the first place!

And because it only works in the long term, most people give up on it and revert to speculating.

But even if you don’t employ it in a valuation tool, understanding the concept is useful.

How do you use it then?

Well, in terms of what we’ve been discussing, it’s very simple.

Say you like a company that you think has a sustainable ROE of 15%. What would be a reasonable price to pay for it?

Well, assuming it pays all its earnings out as a dividend, the equation is very simple. You divide the ROE by the discount rate.

In this case, it’s 15/8 = 1.875.

That is, to get your 8% required return on a company that generates 15% ROE, you would pay no more than 1.875 book value.

However, most companies retain some percentage of their earnings, so there is a compounding effect you need to take into account when estimating value.

This is something I do for my members when recommending stocks. In general, it means the higher the percentage of retained earnings, the higher the valuation.

In reality, all companies need to reinvest some of their earnings to maintain competitiveness and their asset base. If you pay everything out as a dividend and never reinvest, you’ll eventually go out of business.

But some infrastructure-type companies do pay out all their free cash flow as a dividend. Transurban [ASX:TCL], APA Group [ASX:APA] and Spark New Zealand [ASX:SPK] are examples of this.

So, let’s look at what they’re yielding and work backwards. Are investors getting adequate compensation investing at these prices?

TCL trades on a prospective FY25 dividend yield of 5.05%.

APA’s is 6.9%.

And SPK’s is 6%.

That’s not adequate compensation for the risk of investing in a company’s equity if your required rate of return is 8%.

Why is the market pricing them like this then?

There are a few things to consider…

One is that not all investors in the market have the same required return as you. Insurance companies or super funds might have lower return hurdles to meet long-term obligations.

This means they are willing to pay higher prices for stocks, especially for reliable, monopoly type, income producing infrastructure assets like those mentioned above.

Do you really want to compete with investors like this, with deep pockets and very long-time horizons?

For me, these infrastructure companies are too expensive (relative to the current risk-free rate). But for others, their monopoly assets are attractive and worth buying, even though the equity risk premium is thin.

The thinking is that they might be a safer bet than government bonds in an inflationary environment, as they can increase prices and therefore increase dividends.

Better than bonds, maybe. But they have still performed poorly in the post-COVID inflationary environment.

Since 1 July 2020, APA’s share price is down nearly 25%, TCL’s is down about 10%, while SPK has increased around 2%.

Given the ASX200 is up around 30% over the same period, you can see these companies have underperformed significantly. They are clearly trading like bond proxies.

In a rising rate environment, they will struggle. In a falling rate environment, they will do well.

The fact of the matter is that in bullish markets like we’re in now, there are not many companies that offer adequate compensation over and above the risk-free rate.

There are definitely opportunities, they are just few and far between.

By way of explanation, have a look at the S&P500. It trades on a forward P/E multiple of 20.9 times. That translates into an earnings yield of 4.8%.

Compared to a 10-year bond yield of around 4.6%, that’s a skinny ERP.

But here’s a spanner in the works to consider. This is why the market is endlessly fascinating. Companies get the benefit of compounding via reinvested earnings, while bonds do not.

The US tax system does not advantage dividend payments like ours does with franking credits. So companies retain earnings in the US far more than they do here.

I would therefore argue that the US ERP should be skinnier than ours due to this compounding effect.

How much skinnier I don’t know.

But I do know (or at least think) that right now it seems a little too thin. Consider that the last time the US 10-year bond yield was at current levels was back in early November 2023.

At that time, the S&P500 was 13% lower. Yes, it seemed more risky back then. But as I said, that’s how markets work.

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Rumours abounded yesterday that Hong Kong is on the verge of approving new spot Bitcoin ETFs.

If true, it opens up Bitcoin [BTC] to Chinese institutions (and individuals) for the first time since it was banned in 2019.

This is just one of many catalysts set to hit Bitcoin and the wider crypto market over the next few months.

I’ve just released a special presentation on EVERYTHING you need to know.

If I’m right, you’ve a limited window of opportunity to claim your stake in this fast-evolving space before it’s too late.

And when I say limited…I mean just three days from now.

That’s when the ‘Bitcoin Halving’ is due to take place; an event that’s hardwired into the bitcoin algorithm and which halves the new supply of newly mined BTC.

Now nobody knows what could happen this time around, but historically, new all-time highs in Bitcoin along with many other altcoins have ensued in the following 18 months.

And while of course I believe crypto is an investment for way beyond the Halving event…it is a dead-set, guaranteed occurrence that gives anyone interested a clear and renewed sense of urgency.

The time to get interested is now. And that’s what my new presentation is all about.

But for today’s piece, I want to give you a brief taste of the big picture behind these imminent changes.

It’ll help explain China’s about turn on crypto, as well as why some major banks are now buyers too.

Let me explain…

An old Russian warning

I once read a story about an old Russian worker.

His son — who fled Russia in the ‘90s to find opportunity in the west — recalled how his father worked his whole life in Soviet Russia, surviving various upheavals and hardships.

The careful father diligently put aside a bit of money every week to save for a modest retirement.

Unfortunately for him, just as he was about to retire, the Soviet Union spectacularly fell apart.

In 1992, Russian inflation hit 2,500% and continued at high levels for the next three years.

The old man saw a lifetime of savings wiped out in the blink of an eye.

And, as his son dryly noted, he ended up just buying a ‘good pair of shoes’ with his entire retirement fund!

This is an extreme example of how currencies can collapse in an instant.

But the truth is, all currencies slowly devalue over time and all currency regimes come to an end.

Right now, on that front, things are getting very interesting…

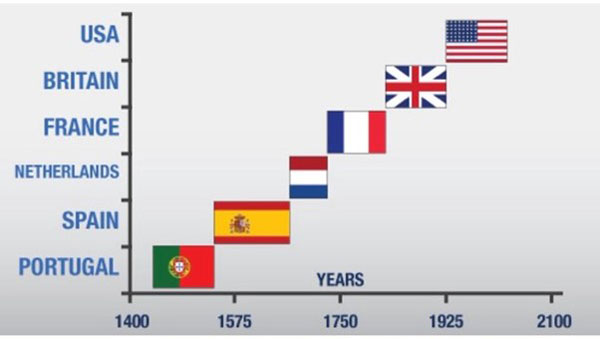

Throughout history, the global reserve currency has changed with the fortunes of the various empires that held power.

Right now, the US dollar holds this reserve status.

And while I’m not saying that’ll change overnight — though I’ll bet the citizens of Soviet Russia didn’t see their collapse coming so swiftly either — there are signs this current regime is in its death throes.

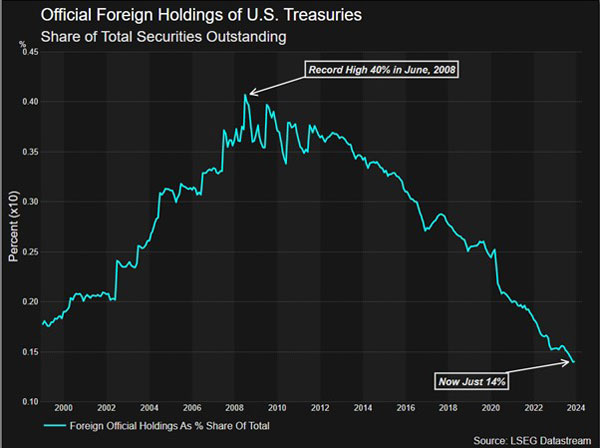

This chart shows the buying of US Treasuries (US government debt) by foreign central banks.

As you can clearly see, they’ve been reducing their holdings of US government debt continuously since the 2008 GFC.

Though, I should point out that foreign private banks and individuals have filled in some of this gap.

Still, it’s an interesting fact to note.

At the same time, central banks are loading up on their gold purchases.

As Mining.com reported this week: